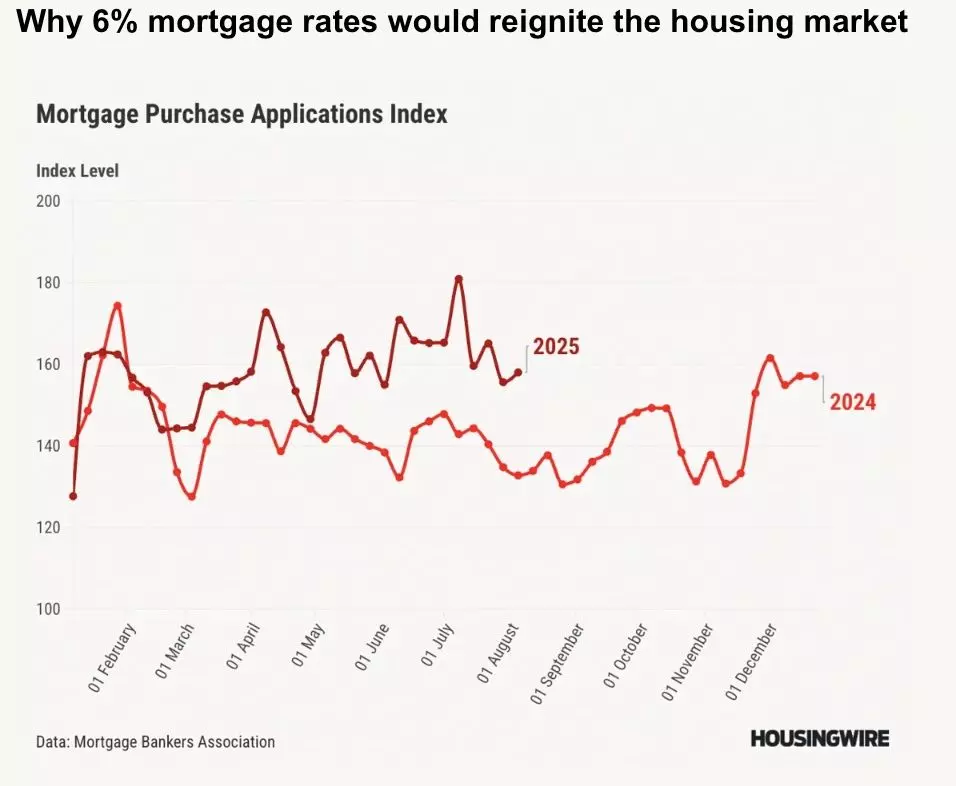

Mortgage Rates Hit 6.57%: Why I’m Still Waiting for 6%

Now that mortgage rates have reached a year-to-date low of 6.57%, many people are wondering if this is the drop we’ve all been waiting for. While 6.57% is certainly a welcome improvement, it doesn't quite have the same impact as breaking the 6% barrier. From my perspective at eXp Realty, and based on what we see in the market, there's a significant difference between a rate in the mid-6s and one that starts with a 5.

Why 6% is the Magic Number

The 6% mark isn't just an arbitrary number; it represents a psychological and financial tipping point for many potential homebuyers. For years, the market has been defined by the "lock-in effect," where homeowners with historically low rates from the pandemic era (often below 4%) are reluctant to sell because they'd have to trade their low rate for a much higher one. This has kept inventory low and prices high.

A drop to 6% or lower is expected to unlock a significant amount of pent-up demand. A recent survey from the National Association of Realtors (NAR) estimates that if rates fell to 6%, an additional 5.5 million households would be able to afford a home. This is a game-changer. It would bring back many buyers who have been on the sidelines, leading to a much-needed increase in market activity.

The Difference in Buying Power

Even a small change in a mortgage rate can have a substantial impact on a buyer's purchasing power and their monthly payment. Let's look at a simple example.

Imagine a buyer is looking at a home with a $400,000 mortgage.

-

At a 6.57% interest rate, the monthly principal and interest payment is approximately $2,544.

-

At a 6% interest rate, that same payment drops to about $2,398.

That's a savings of $146 a month, or nearly $1,750 a year. Over the life of a 30-year loan, that's a difference of over $52,000. For many families, this monthly savings can be the difference between a comfortable payment and one that feels too strained. It allows them to afford a more expensive home, build up their savings, or simply have more financial flexibility.

What Does This Mean for the Market?

While the current low of 6.57% is a positive sign of a stabilizing and potentially improving market, it's not the catalyst for a major shift. The market is still characterized by low inventory and hesitant sellers.

However, if rates continue to trend downward and cross into the 5% range, we can expect to see a stronger spring homebuying season in 2026. This would not only bring more buyers into the market but also encourage more homeowners to sell, which would help alleviate the persistent inventory shortage.

As always, my advice remains the same: the best time to buy is when you're financially ready. While we wait to see if rates drop to 6%, remember that a strong credit score and a solid down payment can help you secure a personalized rate that may already be lower than the national average.

Categories

Recent Posts